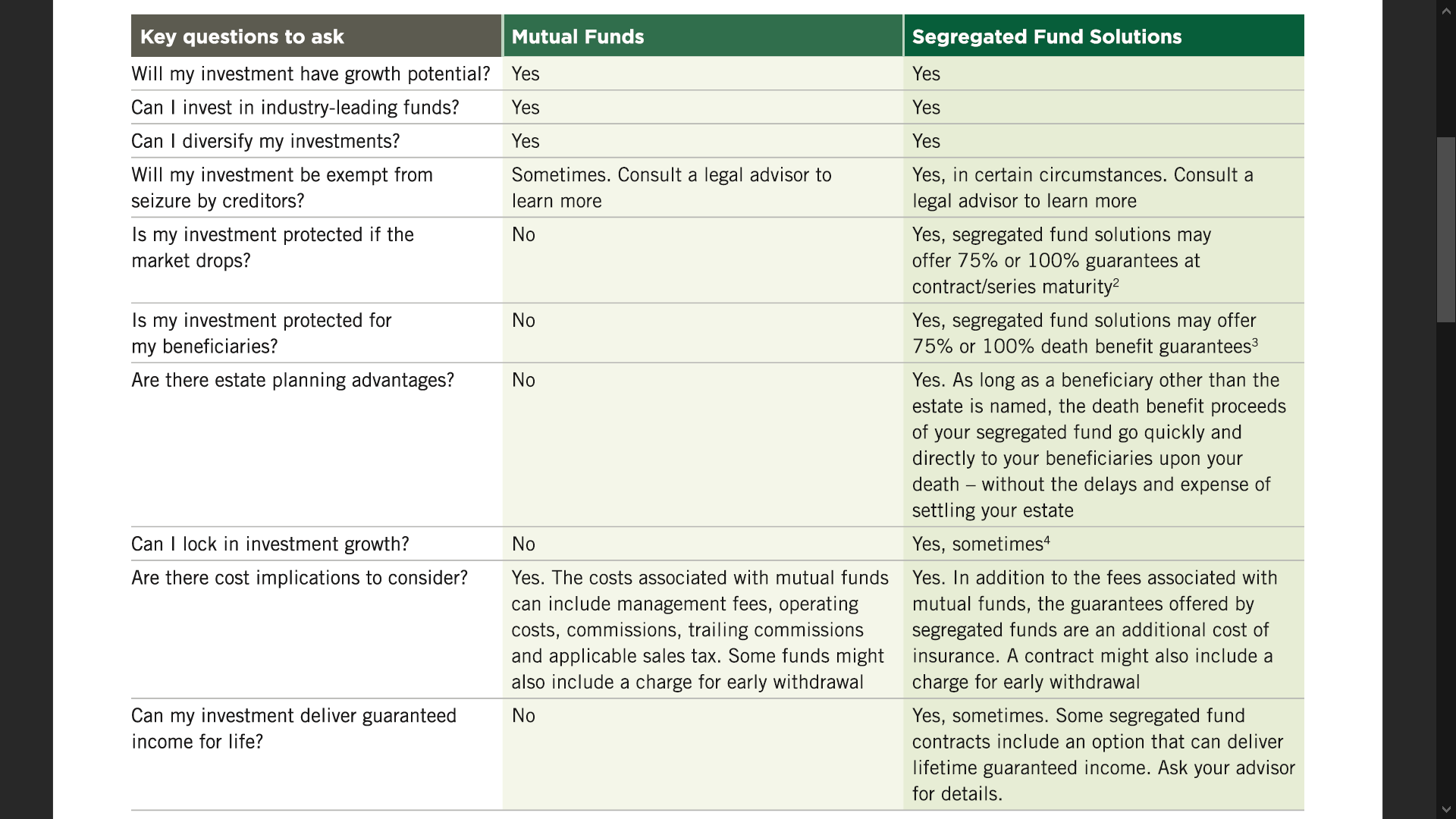

The Best Guaranteed Investment That Withstands The Market Ups & Downs! Part 2

With all these inevitable risks, coupled with the current market condition, it more than ever essential to turn to guarantees and other advantages designed to promote peace of mind. Segregated Fund contracts can be an integral component of a diversified portfolio to ensure that your aspirations and goals for you and your loved ones are achieved with confidence. In addition to access to the growth potential of the markets, investors may take comfort in knowing they can benefit from the following value‑added features:

Maturity Guarantee

At the maturity date, the owner is guaranteed to receive the greater of the market value or the maturity guarantee amount, subject to the provision in the contract or product chosen. This means that in the worst-case circumstance, you’re getting up to 100% of all deposited.

Payout Benefit Guarantee

It guarantees that you get the scheduled income payments provided in the contract, even when the market value is down. In down markets, this guarantee offers additional protection, ensuring that your steady income stream is not interrupted.

Death Benefit Guarantee

Upon the death of the last surviving Annuitant, the beneficiaries will receive a guaranteed amount, the greater of the market value or the Death Benefit Guarantee. The death benefit could be up to 100% of all deposits, less any withdrawals.

Guaranteed Income For Life

Some segregated fund contracts include features that can deliver a guaranteed stream of income for your lifetime or a fixed number of years, as desired. With a guaranteed, predictable income for life, you can be confident that you won’t run of money. Income guaranteed, cannot decrease no matter how the investments perform.

Resets to Lock-in Market Gains

This feature work to capture market growth by allowing the owner to periodically lock-in increases in the market value of their segregated fund contracts. Resets may be automatic or client‑initiated with the assistance of a financial advisor, and may impact the maturity guarantee or Death Benefit Guarantee.

Creditor protection

A segregated fund contract has the potential to protect a client’s assets from creditors. This feature is ideal for professionals and small business owners looking to help protect their personal assets from professional liability.

Estate planning benefits

In addition to guarantees, segregated fund solutions offer your estate planning advantages by helping your loved ones receive an inheritance more quickly and may assist investors to leave more to heirs than they would be able with other types of investment products. Since Segregated funds are insurance contracts, death benefit proceeds pass on quickly and privately to the designated beneficiaries (other than an estate) without any legal, estate administration and probate fees.

Canadians, who are focused on securing a financial future for their family, after they are gone, can rest assured knowing that their loved ones will not endure additional stress during those difficult times.

Other Additional

Potential Creditor P

Assets flowing through an estate (which generally occurs when non‑registered assets paid by financial institutions other than insurance companies) may be subjected to creditors of the deceased, which could mean a smaller inheritance for your heirs.

Privacy & Confidential

Proceeds bypassing the estate and paid to the named beneficiary can preserve confidentiality as the application for probate is a matter of public record. The ability to bypass probate saves your named beneficiaries time and money as well as estate fee upon your death.

Quick & Fast

Settling an estate can be lengthy, frequently taking months or even years should the will be challenged. With a named beneficiary, other than the estate, death benefit proceeds of a segregated fund contract can pass directly to the recipient within a month or two and avoid these delays.

Annuity Settlement Option

This option automatically transfers segregated fund proceeds upon death into an annuity, in accordance with the terms chosen by the client. You also have the opportunity to replace a lump sum death benefit with smaller scheduled payments while providing savings you legal, estate administration and probate fees. It offers additional privacy and potential creditor protection. For heir(s) with poor money management skills or minors, this option comes in handy to spread the inheritance whiles you’re away, at no cost to you!

Want to learn more about Guaranteed Investment Funds and how it can complement your current financial plan, to help you achieve your aspirations and dreams with peace of mind? Connect with us virtually

The Best Guaranteed Investment That Withstands The Market Ups & Downs.

Everyone would all like higher returns on their investments, but few are willing to assume the higher risk usually associated with higher returns. We are aware the markets move up and down, and likewise, we should learn how to factor in the downturn of the market. Unfortunately, volatility is a 2-way street.

People feel confident about their investments in a healthy market. But when the market turns downward, emotions tend to run high. It’s a smart strategy to factor in the downturn phase in our investment plan. This worry has many Canadians looking for investment or retirement vehicles that will not only position their investments for growth when markets are up but also have the potential to protect their capital when markets drop. Any market drops in the years leading up to, or at the retirement stage, can have a devastating impact on a financial future.

Research has shown, not so surprising, that many of us want higher returns than we can achieve with traditional investments like GICs. However, we are uncomfortable or unwilling to assume the risk that can come with those investments that can help us in current investments like mutual funds and stocks.

Today’s investors, like myself, have a simple list of wants when it comes to our money or wealth. They want to :

(a) build and protect their savings,

(b) provide for loved ones

(c) plan for a steady stream of retirement income

(d) retire with confidence and certainty.

An investment product that gives investment choice and the potential for capital growth, the flexibility for diversification and the security of a guaranteed investment is a “Segregated Fund.”

Segregated Funds are most appropriate if you are looking to grow and protect your wealth now and into the future and potentially pass it on to the next generation tax-efficiently.

Segregated fund contracts offer built‑in features designed to help clients achieve peace of mind whiles participating in markets upturns and protecting your capital in downturns. All of these benefits are not possible with other investment vehicles. They appeal to conservative investors, particularly those who worry about market downturns. Over the past few months, I’ve learned that even aggressive investors still have a conservative side to them. Perhaps, you are in this category as well. They have elements that attract business owners and professionals, who may have concerns about creditor protection. They also provide advantages to anyone looking for strategies to protect an estate for loved ones.

Like mutual funds, Segregated Funds are professionally managed and invested in a portfolio of investments. Many segregated funds invest in brand-name mutual funds. But, unlike mutual funds, Segregated Funds are insured investment products. In essence, they are insurance contracts that offer additional benefits such as principal investment guarantees, death benefit guarantees, creditor protection and other estate planning benefits.

Anyone regardless of age, who’s building a nest egg or saving for the future or retirement, can potentially have their savings/ investments negatively impacted by three significant risks:

Market volatility

People feel confident about their investments in a healthy market. But when the market turns downward, emotions tend to run high. Any market drops in the years leading up to, or at the retirement stage, can have a devastating impact on a financial future.

This worry has many Canadians looking for retirement vehicles that will not only position their investments for growth when markets are up but also have the potential to protect their capital when markets drop.

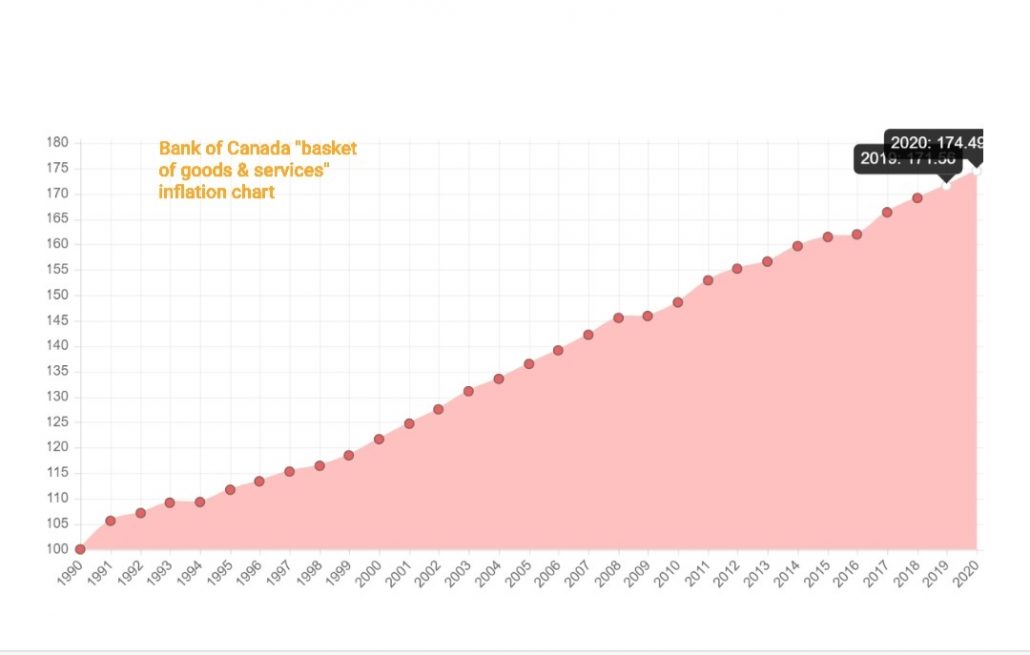

Inflation

Inflation can undermine your portfolio’s purchasing power over the long term. This chart shows how $100 spent on a “basket of goods & services” in 1990 inflates over time. After 30 years of inflation, the cost increase by over 75%. It’s essential to build a financial plan that offers an opportunity for growth, to minimize the effect of inflation.

Longevity

With the advancement in medical breakthroughs, better health care and safer workplaces, we are living much longer. And this could mean that people retiring today may be looking forward to a retirement of three or more decades – almost as long as the working phase of their lives. And more than ever, it’s essential to have a plan that put together ideas to help build sufficient wealth to provide income for a longer lifetime, especially during retirement.

Look out for the conclusion of the article in my next blog, Part 2…

3 Key Essentials To Build a Thriving Legacy

As a small-business owner or entrepreneur, you’re responsible for two families basically; the one you have at home, and the one you have through work.

No matter what your business is, you ought to manage any potential risk(s) you might face in running a successful business or profession. A well thought-out insurance risk management, and benefits program is essential.

For a business owner or entrepreneur, your greatest and a vital asset is most probably You! Your creativity, ingenuity, and management abilities are linked to the survival of the business; starting from now and into the future. Starting a venture that a lot of gut; it’s a risker game and the at the same time rewarding when you see the fruits of the labour.

Unfortunately, running the business has an intrinsic risk associated with it and you have to put in risk managing measures to ensure your brain-child thrive through the various metamorphosis of the business cycle. If you or your business partner die or become disabled, have the right plan and strategy in place would help protect your family and your business in a time of uncertainties.

To get a better sense of how well you’ve planned for these responsibilities, try asking yourself these questions:

- What will happen to my business and family if I die or become disabled- and unable to work?

- What will happen if certain key employees die or become permanently disabled?

- How can I attract and retain the best employees?

- How can I help ensure that my business will be able to weather unforeseen financial hardships?

- What will happen to my business when I retire? (At least plan 10-15 yrs in advance)

Let’s explore and learn more about how risk management strategies can help protect your business while giving you a competitive edge.

Business Continuation Strategies.

One of the first things any business owner needs to consider is how to protect against events that may threaten the future of the business, like the death or disability of a founder, co-founder, partner or key employee. Let me address a few major most business owners, entrepreneur and professional never get time to consider and address;

Income Replacement

Disability – income replacement insurance helps protect your income if you become disabled and can’t work. This is a must-have plan especially for self-employed, independent contracts, business owner and professional who relies on their ingenuity and creativity to earn an income to support themselves and their “two families”. Whether you need to secure their main source of income or supplement the coverage you receive from your employer or an association, Income Protection can help by providing a comprehensive and portable plan they can rely on throughout their working years. There are specialty business protection solutions available for small business owners and entrepreneurs.

Key Person Protection

“Key Person” insurance is another essential component of a smart business continuation plan. Key person insurance protection can be a life or disability insurance purchased by the business on such a key employee (“the Steve Job” kind of employee or partner) and payable to the business. When a key person dies or becomes disabled, insurance can help make up for lost sales or earnings or cover the cost of finding or training a replacement. The cost of hiring and training a valuable employee can be astronomical, especially in those rough times.

Buy-Sell Agreements Funding.

Individuals in business together most often have a shareholders’ agreement that addresses how the shareholders will conduct their affairs and the rights and/or obligations of all of the parties involved. Some shareholders may want to sell, and the others may want to buy their shares should one leave the company either by choice, retirement, disability, or death.

Why are these agreements so important? You might think that if you die, your family could maintain their income by running the business themselves or by hiring someone to handle the day-to-day management. The fact is, your loved ones may not have the skills or the desire for the job, and your co-owners may not welcome the idea of an unintended partner. With a properly structured and funded buy-sell agreement, your business partners won’t have to scramble to come up with the money to buy out your share of the business, and you’ll be guaranteed that your survivors will be compensated fairly and promptly.

Buy-sell agreements are typically funded by life insurance policies purchased on the lives of each of the business owners. You can enter into a buy-sell agreement at any time, but it often makes sense to do so when a business is formed or when new owners are brought into the business with help of a lawyer and small business insurance expert. Because business values can fluctuate, it’s important to review the contract with your accountant at least once per year or to include a calculation method in the agreement. Also, be sure the insurance coverage funding the agreement is up to date.

Clauses can be inserted to insure against the risk of becoming disabled and unable to work. In this case, disability income buyout insurance would fund the buy-sell agreement, allowing the disabled owners to be bought out, typically after a one-year waiting period, when faced with a terminal illness or as agreed by the partner in the shareholders’ agreement.

Let’s know if there any way we can help your business; to ensure you have the utmost peace of mind – we work and coordinate with Accountants and Lawyers, to securing and protecting your legacy, reach us here

Is more of hard-earned money going to your loved ones or the government?

A comprehensive financial plan covers every area of your financial life, from investments and real estate to insurance risk mitigation, retirement planning, and tax and estate planning.

There are a number of financial planning areas that a financial plan may take into account; all based on your current unique circumstances and where you want to be later in life, and what do you want to happen should life uncertainty throw a curve-ball at you or a loved one(s).

While nobody likes thinking about it, planning for a future after you’ve passed away is an important process to go through for your family’s sake. It is essential if you don’t want your loved ones to face financial or legal distress after you’re gone. But that’s exactly what could happen if you don’t make the effort beforehand to put your estate in order.

But there’s good news. It may be easier than you think to get your affairs in order so that the people and/or organizations you care about most will benefit from the estate you have created over your lifetime.

It’s very important to review your estate plan to ensure it continues to reflect your wishes and desires going forward, while still making maximum use of potential tax-reduction strategies available.

Courtesy: AGF Management Ltd -Personal Finance

Six financial planning tips for business owners

Set your business up for success today and develop a financial plan for retirement

Here are six tips for financial success.

1. Target top talent

You want great employees that will help support your business success. These days, steady work and reasonable wages aren’t enough to attract and retain the best talent. Employee benefits can help give you a competitive edge in the marketplace.

2. Find great rates

You want your money to work for you as much as possible. Look for banking solutions that help reduce borrowing costs and that earn the highest possible returns on all your short and long term investments.

3. Find tax efficiencies

Most business transactions–from employee compensation to business succession planning and asset protection–have tax consequences. Understanding and addressing tax implications can make a difference to the success of your business and the growth of your personal wealth.

4. Insure your human capital

Most small businesses have at least one person who is critical to the company’s operations—this could be anyone who helps run the business and is hard to replace. A loss or injury to key personnel could have far-reaching effects on the business’s survival; consider protecting yourself and others with Key Person Insurance.

5. Think future – yours and your business’

Many business owners rely on the sale of their business to fund their retirement and some are concerned with their business continuing after they leave. Combining succession planning with retirement planning can help you enjoy a financially secure retirement–whether you plan to sell or pass the business on.

6. Protect yourself and loved ones

In the case of critical illness, disability, or premature death, the impact on your family’s savings and lifestyle could be significant. Life and Living Benefits insurance products can help mitigate these risks.

- Source: Manulife Financial; read more

How to plan around the small business tax changes, effective 2019

Starting this year, 2019, incorporated private business i.e. Canadian

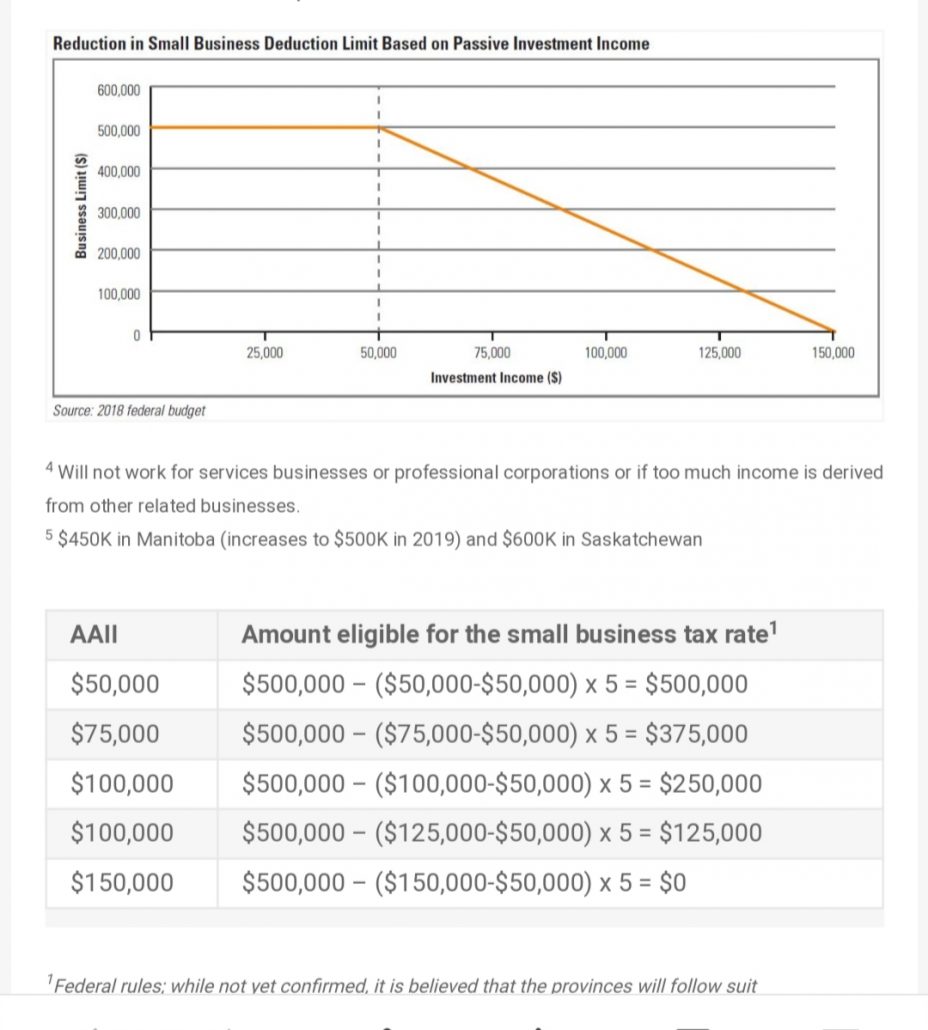

Controlled Private Corporations (CCPC) are taking a different approach when planning their tax and investment optimization strategy to managing their wealth and fortifying their legacy. However, because the reduction will be based on “Adjusted Aggregated Investment Income” (AAII) from the previous year, passive income for 2018 can impact the 2019 small business limit.

Passive income earned inside a corporation e.g. retained earnings, investment income ( such as interest, portfolio dividends, and taxable capital gains) in a Canadian active business can lower a corporation’s small business deduction (SBD). This reduction begins when a corporation (or a group of associated corporations) earns $50,000 of passive income in a year. Specifically, where passive income – known as “Adjusted Aggregated Investment Income” (AAII); exceeds $50,000 for a given year, the corporation’s access to the small business tax rate (10% federally) for the following year will be reduced.

The small business deduction (SBD) will be fully eliminated when passive income reaches $150,000. For each dollar of passive income over $50,000, the SBD will be reduced by $5. That’s once AAII reaches $150,000, none of the corporation’s active Business Income (ABI) will be ineligible for the small business rate and instead will be taxed at the general corporate rate, as illustrated in the graph. Courtesy by CI Investments.

The following strategies can reduce the impact of the new passive investing rules;

1) Invest

2) Buy and hold to defer capital gains

3) Consider corporate-owned tax-exempt life insurance

4) Pay sufficient salary to maximize RRSPs & TFSAs

5) Consider establishing an Individual/Personal Pension Plan (IPP/PPP)

Download to the document below to learn more!