How to plan around the small business tax changes, effective 2019

Starting this year, 2019, incorporated private business i.e. Canadian

Controlled Private Corporations (CCPC) are taking a different approach when planning their tax and investment optimization strategy to managing their wealth and fortifying their legacy. However, because the reduction will be based on “Adjusted Aggregated Investment Income” (AAII) from the previous year, passive income for 2018 can impact the 2019 small business limit.

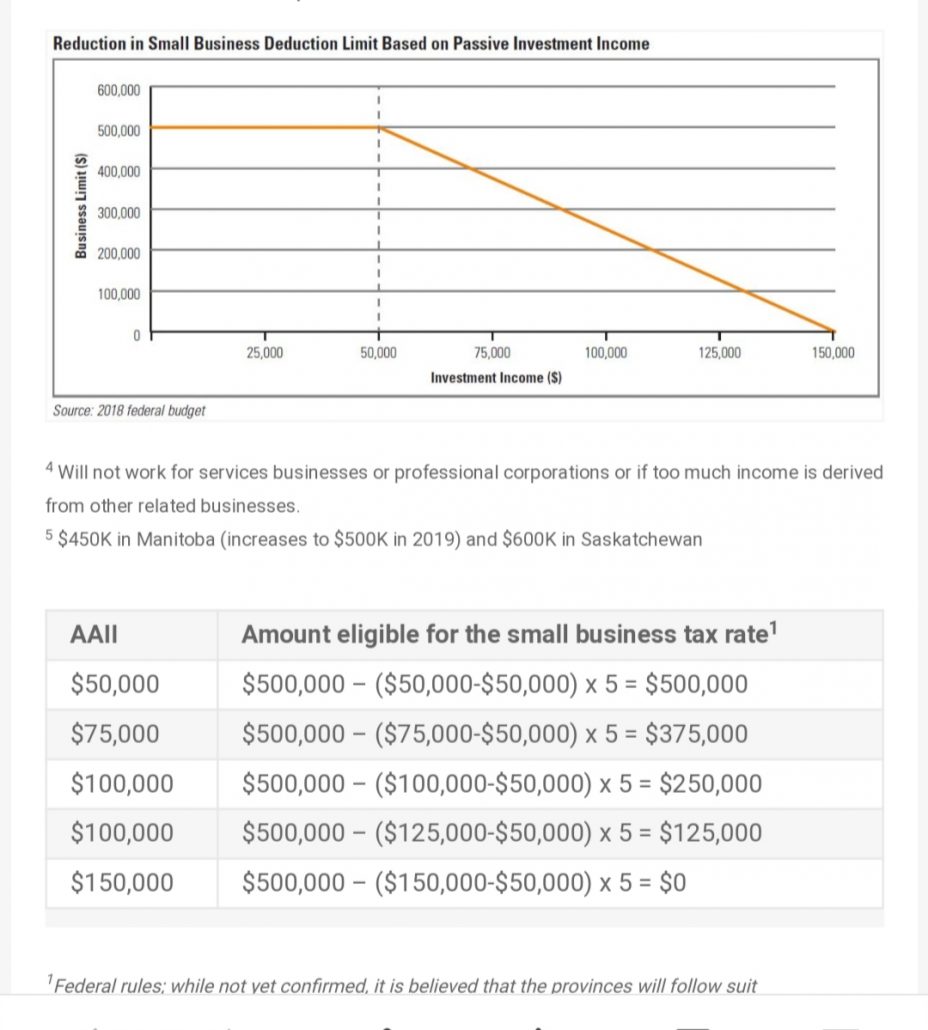

Passive income earned inside a corporation e.g. retained earnings, investment income ( such as interest, portfolio dividends, and taxable capital gains) in a Canadian active business can lower a corporation’s small business deduction (SBD). This reduction begins when a corporation (or a group of associated corporations) earns $50,000 of passive income in a year. Specifically, where passive income – known as “Adjusted Aggregated Investment Income” (AAII); exceeds $50,000 for a given year, the corporation’s access to the small business tax rate (10% federally) for the following year will be reduced.

The small business deduction (SBD) will be fully eliminated when passive income reaches $150,000. For each dollar of passive income over $50,000, the SBD will be reduced by $5. That’s once AAII reaches $150,000, none of the corporation’s active Business Income (ABI) will be ineligible for the small business rate and instead will be taxed at the general corporate rate, as illustrated in the graph. Courtesy by CI Investments.

The following strategies can reduce the impact of the new passive investing rules;

1) Invest

2) Buy and hold to defer capital gains

3) Consider corporate-owned tax-exempt life insurance

4) Pay sufficient salary to maximize RRSPs & TFSAs

5) Consider establishing an Individual/Personal Pension Plan (IPP/PPP)

Download to the document below to learn more!

Leave a Reply

Want to join the discussion?Feel free to contribute!